Trustpilot’s slogan is “reviews you can trust.” Here’s a test of that claim: five companies that pay for a Trustpilot subscription carry strong-to-excellent scores, and are simultaneously the subject of federal settlements, active lawsuits, or complaint patterns alleging the kind of deceptive practices that would make most people think twice before handing over a credit card number.

Each case is verified two ways: the actual Trustpilot profile, confirming the paid-subscription badge and the score, matched against a real regulatory filing, settlement, or court docket – not a forum complaint or an anonymous claim. Time and again, the pattern holds: a paid subscription, a high score, and the very red flags that score was built to catch.

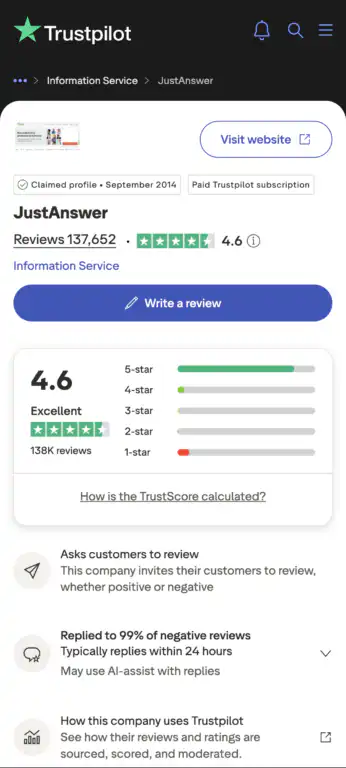

JustAnswer: 4.6 Stars, “Excellent”

JustAnswer holds a paid Trustpilot subscription, has racked up over 137,000 reviews, and sits at 4.6 stars, “Excellent,” with new reviews arriving constantly.

In January 2026, the FTC sued JustAnswer and its CEO, Andrew Kurtzig, directly. The complaint alleges the company advertises access to expert advice for as little as $1–$5, then enrolls consumers in recurring monthly subscriptions ranging from $28 to $125 without the clear disclosure or consent required under the Restore Online Shoppers’ Confidence Act (ROSCA). The lawsuit is still active.

BBB complaints back up the pattern in granular detail: one customer was charged $250 beyond what he’d agreed to; another discovered $368 in charges he never authorized, both only after checking bank statements months later.

JustAnswer’s Trustpilot profile: 4.6 stars, “Excellent,” 137,652 reviews — on a paid subscription, while facing an active FTC lawsuit over its billing practices

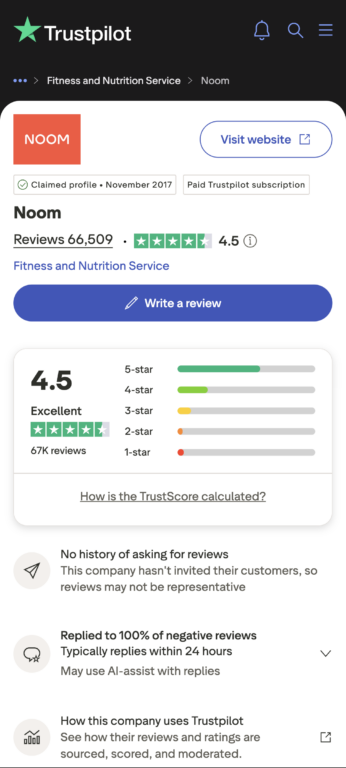

Noom: 4.5 Stars, “Excellent”

Noom, the weight-loss app, holds a paid Trustpilot subscription, has 66,506 reviews, and sits at 4.5 stars, “Excellent.” Its Trustpilot profile flags “no history of asking for reviews.”

In February 2022, Noom paid $56 million cash plus $6 million in subscription credits to settle a federal class action alleging it lured customers with a “risk-free” trial priced as low as $1–$18, then activated auto-renewal and charged non-refundable lump sums of up to $199 – while directing cancellations exclusively through a personal “coach” who plaintiffs said often didn’t respond until after the trial window closed. A former senior Noom engineer was quoted in the suit describing the cancellation process as “difficult by design.”

The BBB separately issued a public warning about Noom in 2020 after receiving over 1,000 complaints describing the same pattern, and the FTC later cited the case directly in its 2021 “dark pattern” policy statement.

Noom’s Trustpilot profile: 4.5 stars, “Excellent,” 66,509 reviews, paid subscription confirmed

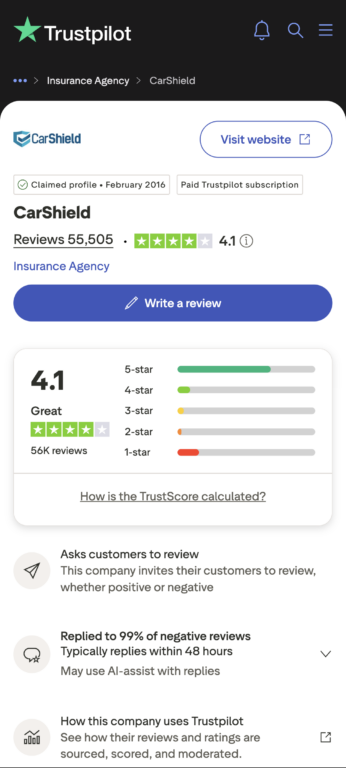

CarShield: 4.1 Stars, “Great”

CarShield, the extended vehicle warranty company, holds a paid subscription, has 55,503 reviews, and sits at 4.1 stars, “Great.”

In July 2024, it and its contract administrator agreed to pay nearly $10 million to settle FTC charges of deceptive advertising – falsely promising, via ads fronted by celebrities including Ice-T, that all repairs to “covered” systems would be paid for, that customers would get a free rental car, and that they could choose any repair shop. In practice, the FTC found, customers routinely discovered the specific repair they needed simply wasn’t covered under the fine print, despite paying $80–$120 a month for what the ads called “peace of mind.” The FTC returned $9.6 million of that settlement to roughly 168,000 affected consumers in December 2025.

CarShield’s Trustpilot profile: 4.1 stars, “Great,” 55,505 reviews, paid subscription confirmed – despite a $10 million FTC settlement over deceptive advertising

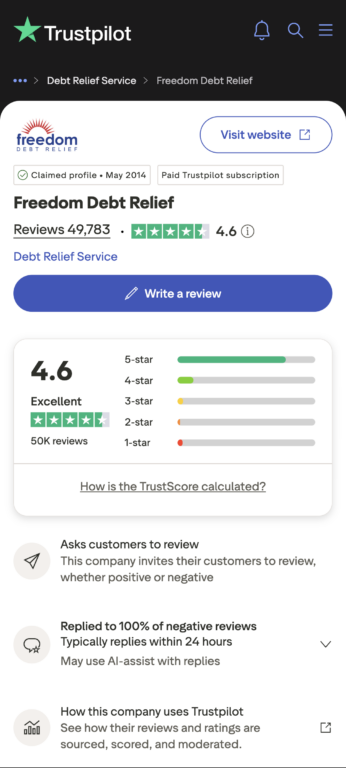

Freedom Debt Relief: 4.6 Stars, “Excellent”

Freedom Debt Relief, the largest debt-settlement provider in the country, holds a paid subscription, has 49,780 reviews, and sits at 4.6 stars, “Excellent.”

In 2019, it paid $25 million to settle a CFPB lawsuit alleging it marketed its “negotiating power” with creditors while knowing that major creditors – Chase, Bank of America, and Capital One are named specifically – refuse to negotiate with debt-settlement companies at all, leaving customers to negotiate alone despite being told otherwise.

The CFPB also found Freedom charged its full 18–25% fee even when no actual settlement occurred, and failed to disclose customers’ right to reclaim their deposited funds if they withdrew. Then-CFPB Director Richard Cordray put it plainly: “Freedom took advantage of vulnerable consumers who turned to the company for help getting out of debt.”

Freedom Debt Relief’s Trustpilot profile: 4.6 stars, “Excellent,” 49,783 reviews, paid subscription confirmed – despite a $25 million CFPB settlement over deceptive debt-settlement practices

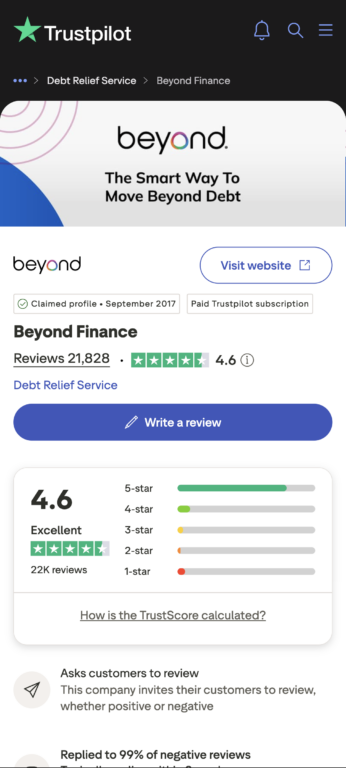

Beyond Finance: 4.6 Stars, “Excellent”

Beyond Finance, a debt settlement company, holds a paid subscription, has 21,827 reviews, and sits at 4.6 stars, “Excellent.”

Unlike the others, it hasn’t yet settled with a federal regulator – but it’s named in a rapidly growing stack of federal lawsuits alleging illegal advance fees and deceptive promises about how much debt it could actually eliminate, part of a wider 2026 wave of 15+ new suits filed against debt-relief companies industry-wide.

BBB complaints attach real numbers to the pattern: one consumer reported paying $60,509.70 into the program against an original $109,469.08 debt, only to be told over $43,000 in payments and unsettled accounts still remained – meaning continuing would have cost roughly what the original debt was worth.

Beyond Finance’s Trustpilot profile: 4.6 stars, “Excellent,” 21,828 reviews, paid subscription confirmed – despite a growing stack of federal lawsuits alleging illegal advance fees and deceptive debt-reduction promises

What Happens Without a Paid Subscription

The five cases above raise an obvious question: does regulatory trouble actually hurt a company’s Trustpilot score, or is score more a function of whether the company pays? To test that, it’s worth looking at companies that faced comparable federal allegations – deceptive subscription terms, hidden fees, hard-to-cancel billing – but never paid Trustpilot a cent. If those companies also score well despite the scrutiny, then payment status doesn’t explain much and regulatory trouble simply doesn’t move the needle either way. If they score poorly, the contrast with the five paid companies above is worth taking seriously.

Three companies fit that test cleanly: Shutterstock, Instacart, and Uber. Each faced a federal complaint in roughly the same window as the cases above, over roughly the same category of harm. None of them hold a paid Trustpilot subscription. Here’s how their scores compare to the five paid companies above:

| Company | Paid Subscription | Score | Reviews | Regulatory Action |

|---|---|---|---|---|

| JustAnswer | Yes | 4.6 “Excellent” | 137,652 | FTC lawsuit, active |

| Noom | Yes | 4.5 “Excellent” | 66,506 | $62M settlement |

| CarShield | Yes | 4.1 “Great” | 55,503 | $10M FTC settlement |

| Beyond Finance | Yes | 4.6 “Excellent” | 21,827 | Pending lawsuits |

| Freedom Debt Relief | Yes | 4.6 “Excellent” | 49,780 | $25M CFPB settlement |

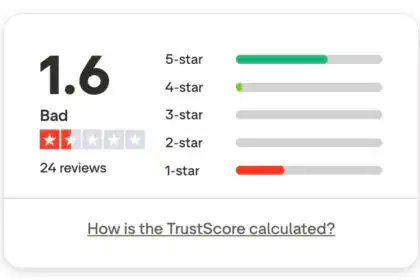

| Shutterstock | No | 1.2 “Bad” | 2,760 | $35M FTC settlement |

| Instacart | No | 1.2 “Bad” | 12,020 | $60M FTC settlement |

| Uber | No | 1.8 “Poor” | 36,536 | FTC + 21 states, active |

What we can see: the three non-paying companies, facing the same category of federal allegation as the five paying companies above, all landed at 1.2 to 1.8 stars – “Bad” or “Poor.” Not one of them broke 2 stars. Meanwhile, every paying company above sits at 4.1 or higher, “Great” or “Excellent,” regardless of whether its regulatory case was a settled fine, an active lawsuit, or still just a pile of pending complaints. Regulatory trouble, on its own, doesn’t seem to move the score much – what moves it is whether the company pays.

Want to understand why this keeps happening? Read the full investigation into Trustpilot’s business model, regulatory record, and one business owner’s firsthand account: Trustpilot Wants Your Reviews to Look Bad – Until You Pay